We’re watching the data roll in each week, and frankly it keeps surprising me. The median price of newly listed homes is climbing, and price reductions continue to fall across the country more quickly than I expected. Inventory was basically flat this week.

Do these early signals of 2023 price support continue into the springtime peak of the market?

Every week, Altos Research tracks every home for sale in the country. We analyze all the pricing, supply and demand, and changes in that data, and we make it available to you before you see it in the traditional channels.

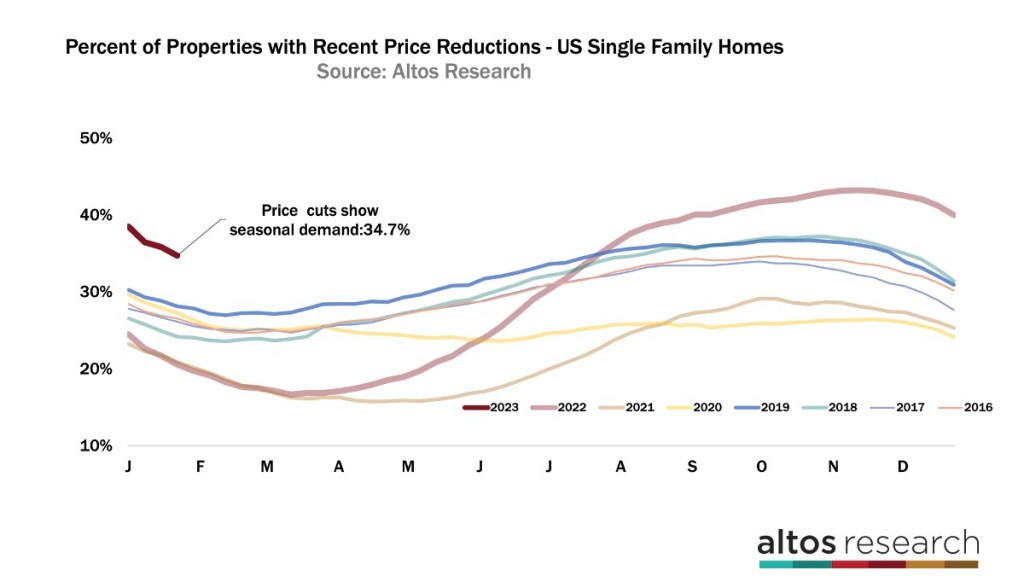

Price reductions fall

Let’s start this week with price reductions. The percentage of single family homes on the market that have taken a recent price cut fell again this week to 34.7%. That’s 1.1% fewer than just last week. It is normal for price cuts to decline in the first quarter of course.

New inventory gets listed, and new listings don’t cut prices until they sit around for a couple months. We also have the first of the spring buying season, so turnover of some that were on the market last fall, took price cuts, are now taking offers too. So it’s normal for price cuts to decline in January.

You can see at the left end of the chart that after last fall we have more of the market now with price cuts than any recent year. Each line here is a year.

Price cuts decline in the first quarter, then pick up in Q2 to peak later in the year. Last year’s market slowdown left us with more of the market having to cut their prices than any recent year.

Now, buyer demand seems to be sufficient that homes are selling with fewer and fewer needing a price cut each week. A normal range for price cuts over the last decade is about 30-35% of the market at any given time. You can see we’re just inside that normal range now.

This is showing more buyer demand that anticipated, especially since mortgage rates are still above 6%. If you have buyers or sellers on the fence this implies more activity and more opportunity. In the fall things were scary as rates over 7% had the market frozen. The market, across the country is significantly less frozen now.

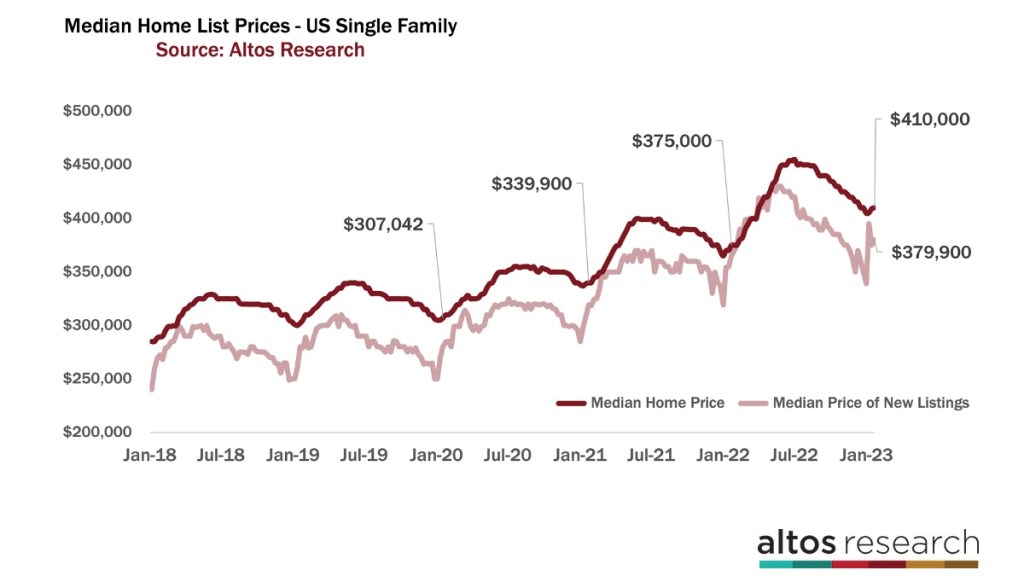

Market resiliency in asking prices

You can see the market resiliency in the asking prices and the leading indicators for the housing market. The median price of single family homes across the country ticked up again this week to $410,000. That’s just a quarter percent higher than last week.

Last year at this time, home prices were accelerating very quickly with bidding wars and over bidding all over the place. So, even as home prices are climbing now, which is normal for January, they’re climbing less quickly than last year, so the year-over-year price change is compressing. Home prices for most of the country have plenty of gains locked in from the last few years. Home equity is very very strong.

Even if you assume a recession still hits later in the year, American home owners are in a really strong financial position. The market is not getting weaker at this time.

Median price of newly listed homes climbed

The median price of the newly listed homes this week also climbed. This is the time of year when we want to see how steep the pricing of the new listings is. That’s the light colored line here. The market is now past the new year’s holiday reset.

New listings start coming to market for the spring season. This light red line above shows us everything the sellers and the listing agents know about their local markets. They will price each new listing accordingly. I know if the inventory is rapidly climbing in my neighborhood, I need to discount to make sure my home gets attention. The steep incline of the light red line here at the far right end of the chart show us January buyer demand and price resilience for the next few months of home sales.

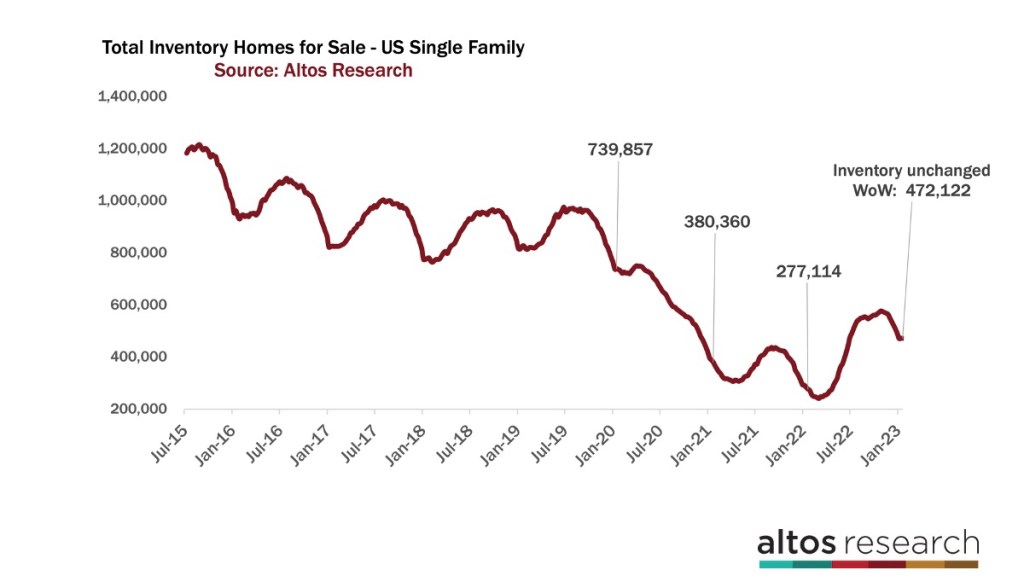

Inventory was flat

Inventory of homes for sale was flat week over week. Actually down just a few hundred homes but lets call it unchanged. It’s perfectly normal for inventory to bounce a little in January but have basically found the bottom before turning up in earnest in February.

The last few years’ inventory kept falling into March or April. Our inventory forecast model expects another basically flat week next week before the February starts to climb.

If inventory keeps falling later in February, that will be a big indicator of a much tighter supply and demand curve that we’ve been expecting. We expect supply to increase in February. But we also know that sellers are being very stingy now, holding on to their existing homes, with ultra cheap mortgages.

If they stay tight and the supply side of the supply and demand curve stays low or declines, that would yet another signal for surprising home price strength this year. We have 36% fewer homes on the market now than we did in 2020 just before the pandemic. That gap is no longer closing.

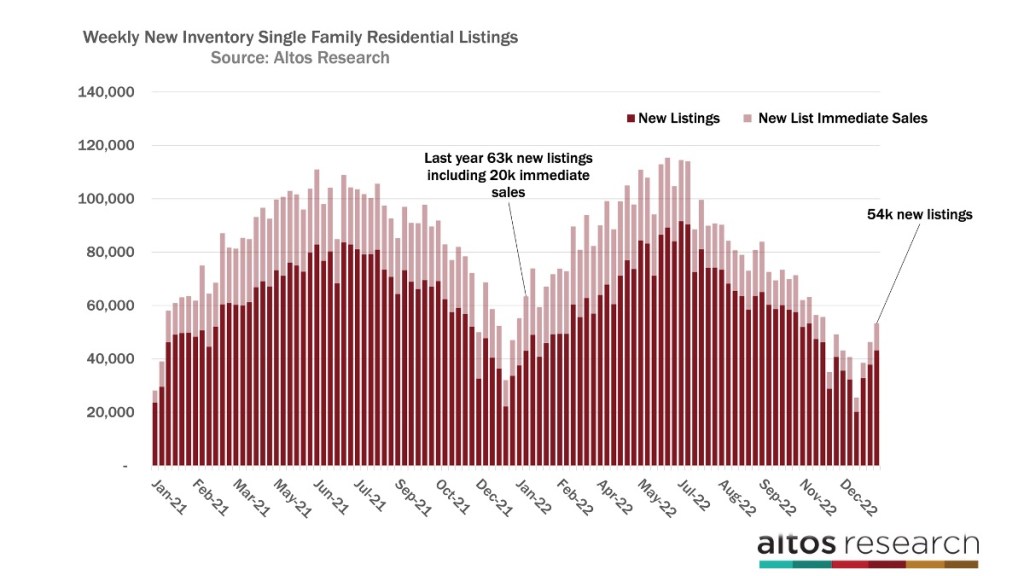

Supply of new listings is low

We had 54,000 new single family listings across the country this week. When last year we had 63,000 new listings is the third week of January. Last year, 20,000 of those went into contract immediately — so then we coupled very tight supply with very high demand. This year we have even tighter supply and low but rising demand.

You can see how new supply should generally keep rising until July 4. You can also see here how we’re on the new low-supply cycle since July 4 last year when we had a dramatic drop in new listings, a step down, from which we have not recovered. Again, it’s hard to be too worried about a big price correction this year when the supply and demand curve doesn’t support it.

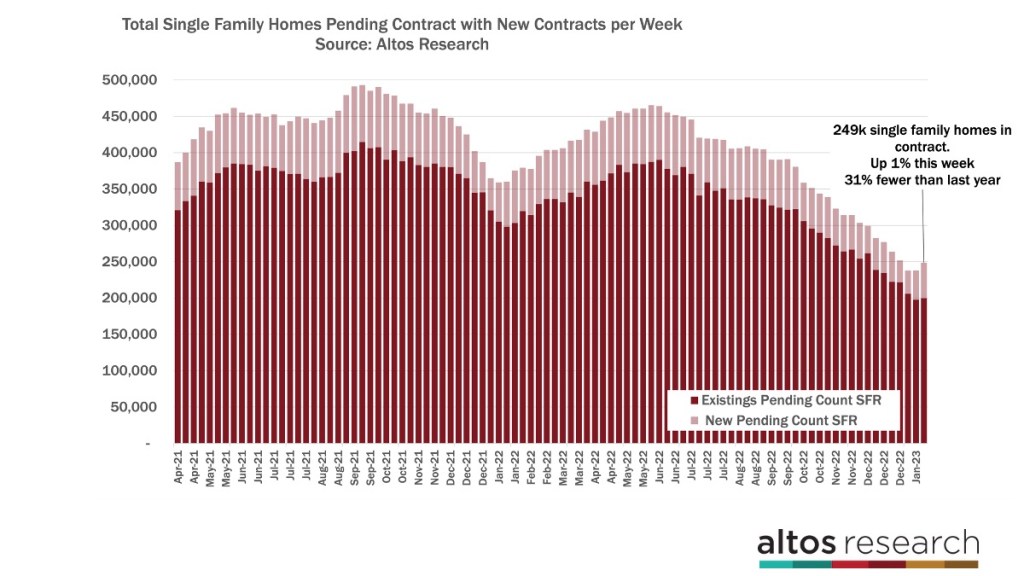

As demand goes, we can see that significantly lower demand in our pendings numbers. We have 249,000 single family homes in the contract pending stage this week. That’s a 1% increase from last week and the New Year’s annual lows. There are 31% fewer homes in contract now than last year at this time. There were 23% fewer new pendings this week than last year at this time.

This tells us that demand is obviously lighter than during the frenzy last year. But that we’re closing the gap that opened up in the 4th quarter.

In the chart above, each bar is a week with the total count of homes pending contract. The light part of the bar are those newly in contract. It’s January so it’s just starting to grow each week. We’re not going to get back to the bidding wars of the last few years any time soon. But this shows us that buyer demand seems to bounced off the bottom.

Because the pendings numbers are so low, these are sales that will complete in the next few months, so those sales headlines will remain low into February and March. It’s a contrast from the green shoots of optimism we’re seeing in the real time data right now.

Mike Simonsen is the founder and president of Altos Research.