In the REAL Trends e-book, Valuing Small- to Medium-sized Brokerage Firms, offers guidance on valuations. Here are two ways to determine value.

There are two recognized approaches to valuing a residential realty firm. They are:

- The Income Approach (EBITDA)

- The Gross Margin or Company Revenue Approach

The Income Approach is the most widely used by buyers and sellers. It’s also recognized in most legal jurisdictions and

by professional valuation organizations throughout the United States.

The Gross Margin or Company Revenue Approach is used when a firm has little earnings performance or is a small firm (less than $2 million in gross revenues). It’s also used when the owner contributes a material portion of the revenues or income of the firm.

While there have been other approaches used at various times in the past 30 years, these two approaches are used by nearly all buyers, whether they’re national, regional, or local, and without regard to the size of the brokerage.

The Income Approach

The Income Approach is the most commonly used approach to valuing a residential real estate services business, including realty, mortgage, title, and escrow services. It’s sometimes referred to as the EBITDA (earnings before interest, taxes, depreciation, and amortization) approach. In this report, we’ll refer to it as the Income Approach.

The Income Approach first determines the income from the business over a certain period and then applies a multiple of that income to determine value.

The most common period used for calculating EBITDA is the most current twelve (12) months of the company’s operations.

Items included in income for this approach include:

- Profit before income taxes;

- Depreciation;

- Operating interest expense (interest on business operating accounts and not interest on buildings or personal assets owned by the owner and carried on the balance sheet of the company;

- Amortization;

- Owner’s compensation and benefits;

- Non-recurring expenses.

Items deducted from the income and considered chargebacks are:

- Comparable costs of management (see definitions in Appendix);

- Non-recurring income;

- Interest or dividend income;

- Owner’s commission contribution to revenue net of any commission paid to the owner

The items are deducted from the income to determine the EBITDA of the firm for a determined period. In the past, this has been either the most current 12 months of results or an average of the last two to three years of these results.

A multiple is then calculated against this income to determine the value of the firm. The multiples vary according to market conditions, location, and size of the firm and other factors that will be discussed further.

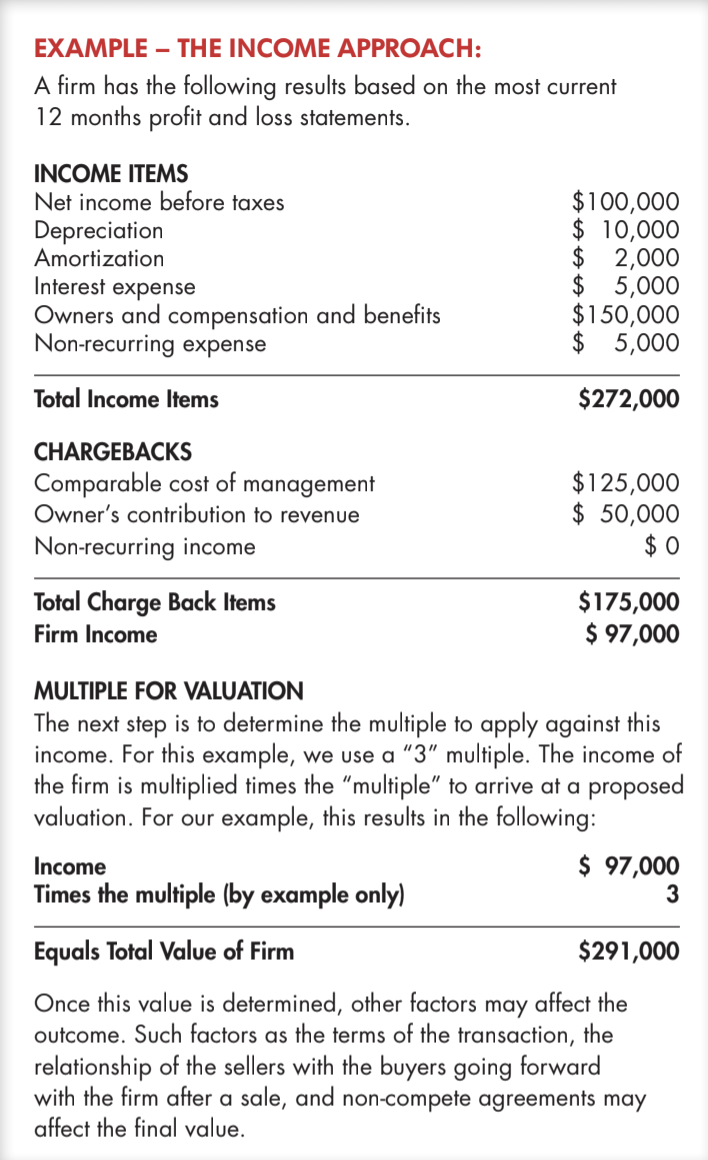

Example –– The Income Approach:

The Gross Margin or Company Revenue Approach

The Gross Margin or Company Revenue Approach is used mostly for firms that have little or no earnings or are small firms to medium-sized companies or where the owner contributes a material portion of the revenues of the firm.

The Gross Margin or Company Revenue Approach examines the company’s revenue for the firm over a period, most often the last 12 months of operations.

Gross Margin or Company Revenue is the sum of revenue that is retained by the firm after payment of all costs related to sales. Such costs as commissions to the firm’s sales associates, referral fees to outside sources, co-brokerage fees to outside brokerage firms, and franchise fees are deducted from Gross Revenues to determine the Company Revenue figure.

Once the Gross Margin or Company Revenue figure is determined, a percentage is applied against the figure to determine value.

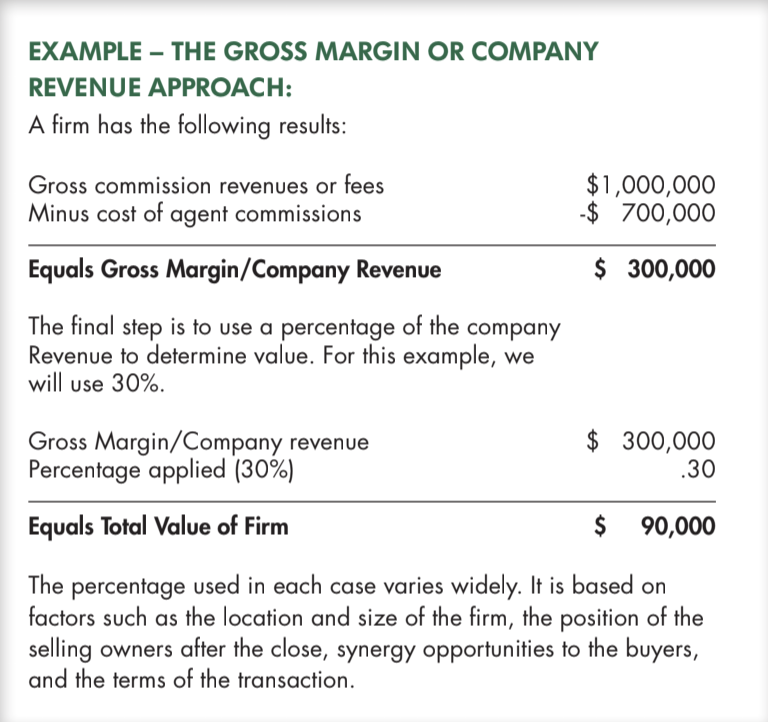

Example –– The Gross Margin or Company Revenue Approach

Composition of the Deal: Cash Versus Earn-Out

It is important to comment here that all cash transactions at the Fair Value are virtually non-existent in the residential brokerage industry. Most residential brokerage company mergers or acquisitions are based on a percentage of the Fair Value in cash at closing with the remainder often in an earn-out or contingent payments over a period after closing.

{{cta(‘93183588-540c-4d8d-8f22-4112185e4738’)}}